The IRS typically has three years after the tax return is filed to audit a return (or much longer for certain returns). Knowing when the IRS statute of limitation on audits expires is one of the easy ways for any taxpayer or business owner to safeguard themselves. If you’re an individual filer or have books to maintain for a growing enterprise, understanding the IRS’ ability to go back will help you understand your exposure and how long you need to hold on to your books. If you’re thinking, “Can the IRS audit old tax returns in my case?” or if you’re juggling the whole complexity of an IRS audit for a small business, then the best move is to seek professional help before trouble even starts.

How far back can the IRS audit a tax return in normal circumstances?

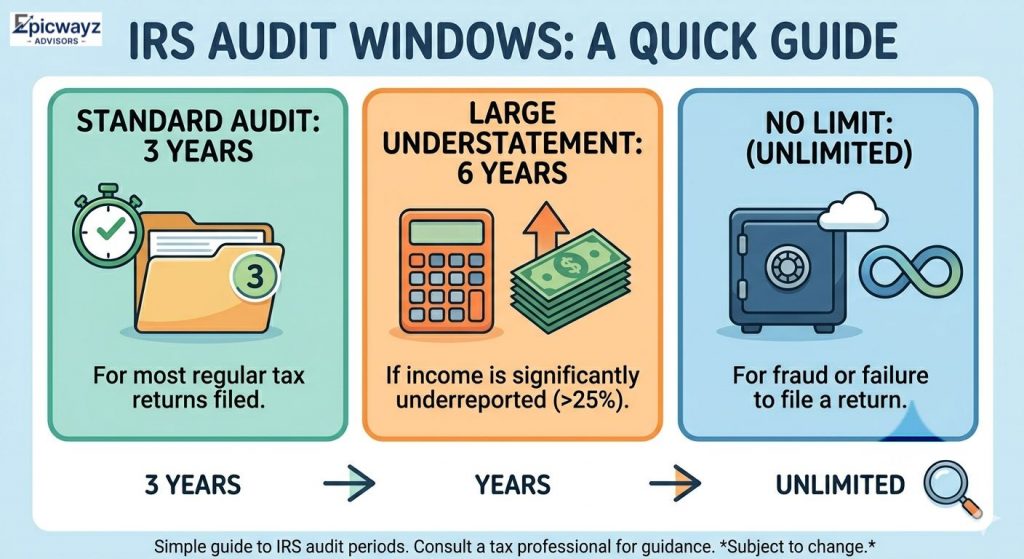

Normally, the IRS has three years from filing a tax return or from the filing deadline to audit a tax return. This is the general rule for most taxpayers who are filing under normal conditions. If you are on time as a filer, accurate as an income reporter and have clean, documented records, then it is the three-year window. After this time, the IRS will not normally reopen the return for inspection. This is why it’s important to know the IRS audit statute of limitations for long-term tax planning.

Be familiar with the Standard Audit Time Limits.

The usual IRS audit time frame is three years from the return’s filing date or the date of return, whichever is later. This is the case when the income is completely reported and there are no major errors. The best protection against the standard limitation period is for timely, accurate and well-documented returns.

Can IRS audit returns that are more than three years old?

Yes — but this is where many taxpayers are surprised. The answer to the question about whether the IRS can audit old tax returns outside of the 3-year limit is a definite yes, but with certain conditions. The three-year rule isn’t absolute, and there are several regularly occurring scenarios that bring the IRS’s history back much further than three years.

Exceptions to the General Audit Rules

- Underreporting of income by more than 25% of gross income — The six-year window applies if the IRS believes you underreported your gross income by 25% or more. This is one of the most probable exceptions that can be triggered and would impact individual filers and those who are concerned about a possible IRS audit for small business owners whose income can vary.

- Foreign financial accounts and assets — Taxpayers with unreported foreign income or hidden foreign bank accounts will have a longer period of time to be audited. International income non-disclosure is an IRS compliance problem, with its own rules and regulations.

- Amended returns — If an amended return is filed, it can restart or extend the audit clock in certain situations, especially in the case of major changes in reported income or deductions made in an amended return that is filed near the end of the existing audit clock.

The IRS may have more time, in excess of the three-year period, to audit a refund claim or a carryback of a net operating loss, so documentation is crucial in these cases.

What does underreporting income do to the IRS audit time frame?

One of the quickest methods to have an audit exposure that lasts longer than the typical 3 years is to under-report income. If the IRS finds that there is a substantial discrepancy between what you reported and what your third-party sources reported on your behalf (such as employers, banks, or your clients), it can go back even further.

What is Extended Statutes of Limitations?

The IRS audit statute of limitations becomes 6 years instead of 3 years if the taxpayer underreports gross income by more than 25%. This is for both personal and business taxpayers. In the case of IRS audit for small business, it’s typically unreported cash income, misclassified income, or failure to account for 1099 income from clients or vendors.

Can the IRS Audit a Taxpayer Indefinitely in Certain Cases?

Yes, for certain serious cases, the IRS audit statute of limitations does not exist. Under some circumstances, the IRS will not have a time limit and returns from any year will be open for examination. This isn’t hypothetical; it’s a reality of enforcement that impacts real taxpayers annually.

Fraud, Tax Evasion, and Unfiled Returns

- The statute of limitations is completely forfeited if there is tax fraud or civil tax evasion. The IRS has no time ceiling on how many years it can audit if it can prove a taxpayer was being dishonest or intentionally filing a false return. One of the most significant safeguards any taxpayer can have is filing an accurate and honest return.

- Statute of limitations does not apply to unfiled tax returns. So, if you did not file a return for a year, that year remains open for IRS examination and enforcement action indefinitely, no matter how long ago it was. The IRS audit statute of limitations does not begin to run until the return is filed.

- Employment tax issues — Non-payment or non-reporting of payroll taxes increases the potential for businesses to be exposed to extended audits. In IRS audit for small business cases involving employee misclassification or unreported employee wages, the IRS may pursue unpaid employment taxes without the normal time restrictions.

That’s where professional assistance can make a difference. Epicwayz Advisors offer a range of Tax Services, Accounting Services, Fractional CFO Services, and Business Advisory Services that are tailored to help individuals and business owners maintain clean, audit-ready books, report income accurately, and remain compliant with IRS requirements every year.

Conclusion

The IRS has more time to audit you than most people realize, and in certain situations, there may be no clear time limit at all. Understanding the IRS audit statute of limitations, maintaining solid records, and filing a complete, truthful return each year are the foundations of smart tax compliance. Epicwayz Advisors also offers specialized guidance, document support, and ongoing tax oversight to help keep your financial situation organized not only during tax season but throughout the year.